September 2023 local market update - Big gain despite the pain

Yes, that’s right, a quick search on google shows that the mortgage rate available today is 8%.

For a $800,000 purchase with a 20% downpayment, your monthly payment 2 years ago at a 3% mortgage rate was roughly $2,700. Today, it’s $4,700. Ouch. And that’s before taxes and insurance.

On top of this, the cost of insurance and taxes have increased dramatically. Insurers pull out of entire states, including Colorado. The remaining insurers are left with less competition, more pricing power and more risk. Regarding taxes, most homes were reassessed this year in our area, leaving homeowners with a 2x or more higher tax bill in their hands.

The market shrugs

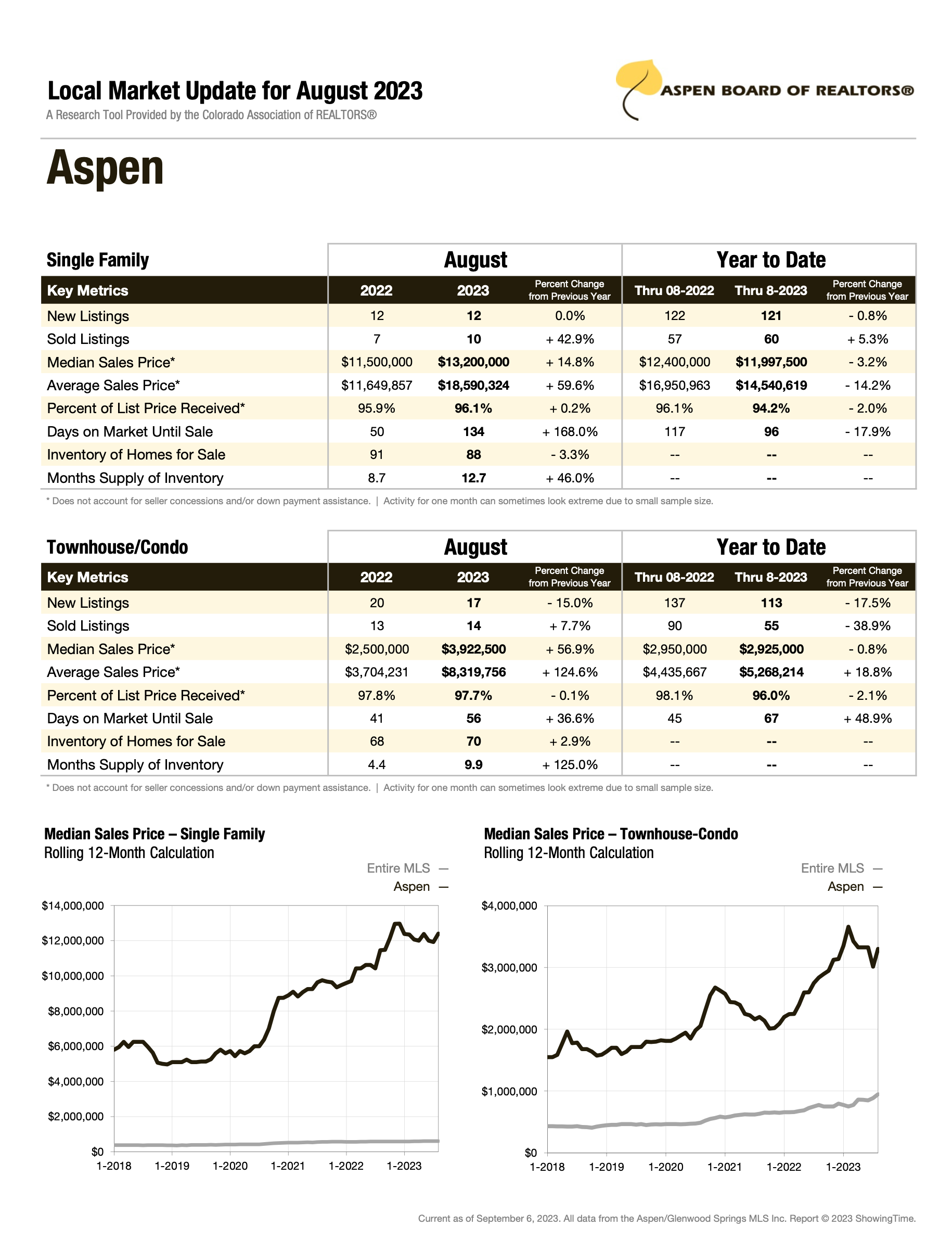

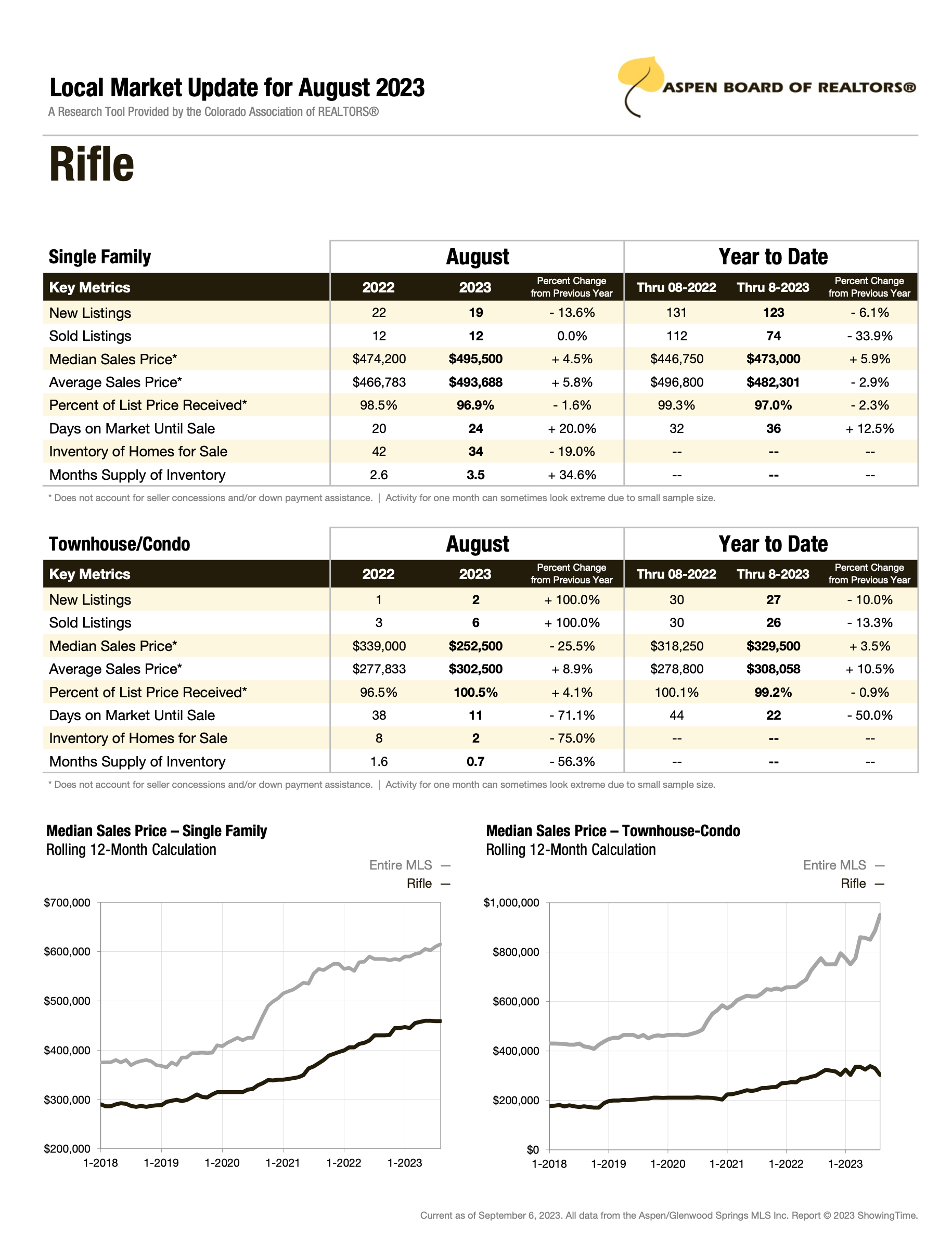

Meanwhile, home prices continued to go up undisturbed! Values are over 32% higher in our valley than they were a year ago. On this month’s stat report from the Aspen Board of Realtors, we see the median sales price up almost 15% in Aspen compared to last year, 54% in Basalt, 83% in Carbondale and 21% on Missouri Heights. The “golden handcuffs” are still in full effect: over 75% of homeowners currently have a mortgage rate of 4% or less on their home. It takes a really good reason to let that go for an 8% mortgage rate your next home. Therefore active listings are down over 23% in our area. You can find the detail per town at the bottom of this article.

The result is simple: prices are on the rise, as counterintuitive as it may seem. Despite the squeeze on homeowners created by higher mortgage rates, higher insurance costs and higher taxes, prices keep going up because of the low inventory. In most other countries (Canada, the UK etc…) there is no 30 year fixed mortgages. Every rate is adjustable. The US government created the 30 year fixed mortgage product to support home values. It seems to work, and maybe too well. Affordability is absolutely terrible in our valley, and there is no end in sight.

Who wins, and who loses?

In these market conditions, the winners are:

the cash buyers who face less competition than before and don’t care what the interest rate is.

People willing and able to sell their home who can yield a good profit on their sale.

Contractors: home improvements should remain strong since homeowners’ mobility is very limited. They will likely decide to improve their current home rather than move to a different one. Home renovations, construction of additions and ADUs should be going strong for a while.

Homeowners with a low mortgage rate locked in: They should see their home value increasing or stabilizing, creating a comfortable cushion of wealth to weather a possible slowdown in the economy.

Unfortunately, some people will lose in this market:

Renters: rents will keep rising as demand for rentals go up when people are not able to buy.

First time homebuyers: they don’t have a home to sell and therefore won’t benefit for high values, while they have to deal with high prices, high rates, high taxes and high insurance cost.

People needing to sell their current home to buy their next one will lose a lot of purchasing power in the process. They’ll have to let go of a low rate for a high one.

Insurance brokers, people working in the lending industry, and Realtors will keep operating in a slow and challenging market for the time being and will see depressed transaction volume.

Please find the breakdown per town below.