Mortgage rates under 7%. Time to dance again? - December market update

The Federal Reserve’s meeting that took place last week marked a turning point. Chair Powel announced the end of this tightening cycle. In other words, interest rates won’t go up for the foreseeable future. Actually the Fed is forecasting 3 rate cuts in 2024. What does this mean for the next few weeks and months?

For now, the future is bright!

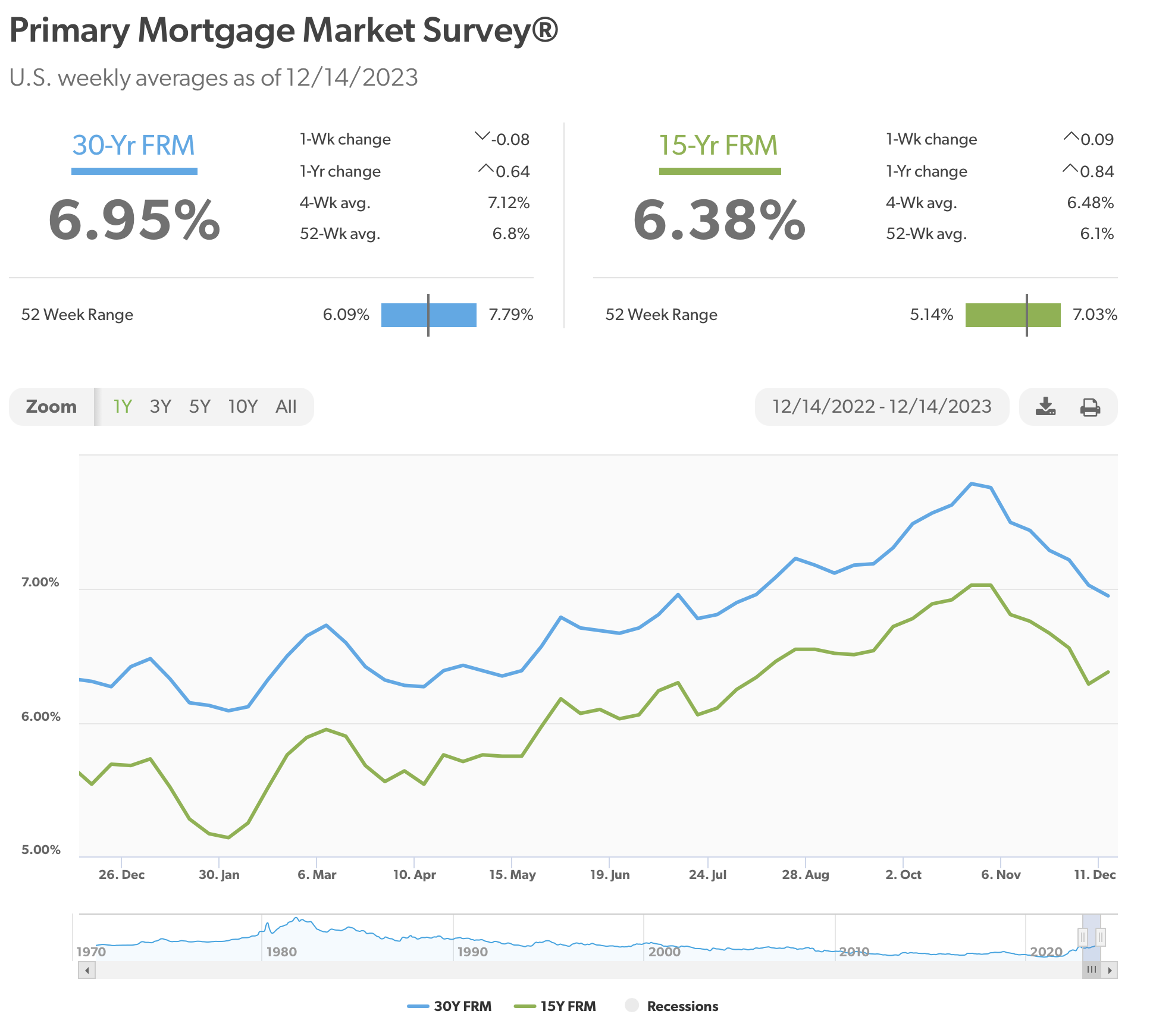

In the immediate future: Rates have already come down! The Federal Reserve sets their rate, and they are only one of the factors at play to determine mortgage rates. In this case, the mortgage rates are already going down as we speak even though the Fed rate remained unchanged. This will bring some air to the market in the depth of the slow season (the hollidays are rarely people’s preferred time to move).

In the next few months: We need interest rates to go down, and unemployment to remain low. Interest rates will remain between 6 and 7% for the next few months - time for the Fed to make sure inflation doesn’t make a come back. Keep an eye on economic indicators, especially employment. The Fed has a dual mandate: ensure price stability and maximum employment. If they decide to cut rates faster than forecasted yesterday, don’t rejoice too much. It’s likely in reaction to something going wrong in the economy and that could affect unemployment, and affect real estate prices negatively. In the meantime, the next few months will be easier on all of us, with conditions stabilizing or easing, rather than tightening.

In 2024 - What is the Fed high rates “break” something? The Fed’s goal is to engineer a “soft landing”. Not to make real estate cheaper. A crash is never intended, but historically when the Fed tightened their policy, something broke in the economy. When interest rates staying high for a while, the weaker parts of the economy start breaking before the Fed is willing to get rates down. Most tightening cycles have ended with a recession. Will it be different this time? Debt levels are at an historic high. I’d argue that whether you believe that a crash will happen or not, having cash reserves is a must in real estate anyways.

2024 - the case for real estate prices continuing to go higher: policy makers usually go too far one way, then too far the other way the next time over. Last time they raised interest rates close to today’s level, the 2008/2010 crash happened, and nobody wants to see a repeat of that. The Fed might be trying so hard to avoid another 2008/2010-type chaos, that they might let things run more than the usual. They might settle for a long term affordability issue and slightly higher level of inflation than their 2% official target.. We might see a “soft landing” that really looks like we are slowly going back to the moon. If their plan works, you will see interest rates slowly going down through the year, prices of homes stabilizing/going up 2 to 5% a year, and employment staying low. If that’s the case, be ready for home prices to go up closer to 5% a year or more in our area, as the Fed eases their rate policy while inflation remains somewhat high. Real estate owners will be the big winners in this scenario.

Affordability is the elephant in the room

There is a crisis going on in real estate right now. It’s not a crash in values, like in 2008/2010. It’s a crisis of affordability. In our area as a whole, the affordability index is at 25, which is extremely low. The effort by the Fed to engineer a “soft landing” means taming inflation down while maintaining asset value. For affordability to improve during a “soft landing”, the price of real estate will have to remain stable while interest rates are going down in a growing economy…. That would basically be a miracle! In our area specifically, the number of buyers sitting on the sidelines waiting for this to happen makes me think that if we dodge a crash during the period of high rates we are going through, we are going to come on the other side VERY strong. Real estate will remain too expensive for most, and wealthy buyers will remain the only game in town. If this market doesn’t cycle downward in 2024/2025, rent rates and prices will continue to eat up the largest part of local people’s income in our area, and the trends that define the current affordability crisis will continue and accelerate.

Breakdown of the latest market local stats per town below: